Partners eInsure

ANNOUNCEMENT:

We have migrated our e-Commerce services to a new platform with a new look and more features to serve you better. Please update your bookmarks to the new URL. Thank you for your understanding and support.

Our office will close at 4.15pm on 13 Mar 2026. Click here for details.

ANNOUNCEMENT:

We have migrated our e-Commerce services to a new platform with a new look and more features to serve you better. Please update your bookmarks to the new URL. Thank you for your understanding and support.

ProtectionPlus is a personal accident insurance plan that offers robust financial protection with a high permanent and total disablement payout of up to $375,000 and covers third-degree burns. The plan includes daily hospitalisation benefits, bereavement grants and value-added covers for riders, reservist training and leisure sports.

With comprehensive coverage and peace of mind, ProtectionPlus allows up to 3 children to be covered under the policy for free - ensuring you and your loved ones are safeguarded against life's unexpected events. Secure your future with our reliable personal accident insurance today.

ProtectionPlus is a personal accident insurance plan featuring a high permanent and total disablement payout of up to $375,000.

We pay a $200* daily hospital cash benefit for a maximum of 50 days if you meet with an accident.

You and your family will be supported with a monthly income of $2,400* for up to 2 years if you are unable to work due to temporary total disablement.

The plan offers a $10,000* bereavement grant, one of the most generous in the market.

Protect your entire family with free cover for up to 3 children when you and your spouse enrol for ProtectionPlus at the same time.

Provide cover for third degree burns arising out of any injury.

*Cover and limits are based on Platinum Plan.

Protect yourself easily by purchasing our personal accident plan online.

We keep our process as simple as possible to bring your personal accident claim to a fair settlement.

Value-added covers for motorcycling as a rider or pillion rider, Injuries during reservist training and leisure sports like snorkelling, wakeboarding and bungee-jumping, plus access to MSIG Assist helpline in the event of an emergency overseas.

| Sum Insured | |||

|---|---|---|---|

| Silver Plan | Gold Plan | Platinum Plan | |

A. Death | $100,000 | $150,000 | $250,000 |

B. Permanent and Total Disablement | $150,000 | $225,000 | $375,000 |

C. Permanent and Partial Disablement (as per table) | Up to $100,000 | Up to $150,000 | Up to $250,000 |

| Sum payable as a % of Permanent and Total Disablement | Sum payable as a % of Permanent and Total Disablement | Sum payable as a % of Permanent and Total Disablement | |

| 1. Loss of one or both arms (between shoulder and wrist) | 100% | 100% | 100% |

| 2. Loss of one or both legs (between hip and ankle) | 100% | 100% | 100% |

| 3. Loss of sight in one or both eyes | 100% | 100% | 100% |

| 4. Loss of sight in one eye except for perception of light | 50% | 50% | 50% |

| 5. Loss of lens of one eye | 50% | 50% | 50% |

| 6. Loss of hearing in both ears | 75% | 75% | 75% |

| 7. Loss of hearing in one ear | 15% | 15% | 15% |

| 8. Loss of speech | 50% | 50% | 50% |

| 9. Loss of four fingers and thumb of one hand | 50% | 50% | 50% |

| 10. Loss of four fingers of one hand | 40% | 40% | 40% |

| 11. Loss of thumb - one phalanx or two phalanges | 20% | 20% | 20% |

| 12. Loss of finger - three phalanges | 10% | 10% | 10% |

| 13. Loss of finger - two phalanges | 5% | 5% | 5% |

| 14. Loss of finger - one phalanx | 3% | 3% | 3% |

| 15. Loss of all toes of one foot | 17% | 17% | 17% |

| 16. Loss of great toe - one phalanx or two phalanges | 5% | 5% | 5% |

| 17. Loss of any toe other than great toe - one phalanx or two phalanges | 3% | 3% | 3% |

| 18. 3rd Degree Burns | from 25% to 100% | from 25% to 100% | from 25% to 100% |

Where the injury is not specified above (other than loss of sense of taste or smell where no compensation is payable) the amount will be determined based on the degree of disablement as assessed by our medical advisors. | |||

D1. Temporary Total Disablement (TTD)Inability to engage or attend to the usual employment or occupation (up to 104 weeks) | $100 per week | $300 per week | $600 per week |

D2. Temporary Partial Disablement (TPD)Inability to engage or attend to the usual employment or occupation (up to 104 weeks) | $50 per week | $150 per week | $300 per week |

E. Worldwide Medical ExpensesIncludes Traditional Chinese Medicine, Accidental Dental and Mobility Aids | $1,000 | $3,000 | $5,000 |

F. Hospitalisation Cash BenefitHospitalisation for at least 24 hours after accident | $50 per day (Max $2,500) | $100 per day (Max $5,000) | $200 per day (Max $10,000) |

G. Recuperation BenefitHospitalisation for more than 14 consecutive days | $100 | $250 | $500 |

H. Bereavement GrantFollowing death by accident | $3,000 | $5,000 | $10,000 |

TerrorismExcluding biological, chemical agents and nuclear devices | Covered up to the Sums Insured on Death at the first inception of the insurance | Covered up to the Sums Insured on Death at the first inception of the insurance | Covered up to the Sums Insured on Death at the first inception of the insurance |

Bonus Cover At No Extra Cost!

10% increased cover for Death and Permanent Disablement each year, up to the 3rd renewal. That's 30% extra cover from the 4th year, absolutely FREE! (if no claim is made in the preceding year)

| Sum Insured | |||

|---|---|---|---|

| Silver Plan | Gold Plan | Platinum Plan | |

A. Death | $10,000 | $15,000 | $25,000 |

B. Permanent and Total Disablement | $15,000 | $22,500 | $37,500 |

C. Medical Expenses | $100 | $300 | $500 |

Cover For Your Child(ren):

| No. | Questions & Answers | |

|---|---|---|

| 1 | What is the definition of an Accident under this insurance? An Accident refers to an event which happens suddenly and gives rise to a result which the Insured person did not intend or anticipate. All benefits are payable under this policy only when it is due to an accident. | |

| 2 | Who can enrol for this insurance?

Provided all persons to be insured are residing in Singapore. | |

| 3 | If I am already insured with another insurer, how can I arrange cover for my spouse and children? Your spouse may apply for this insurance on his/her own. In which case, 3 of your Children can be covered at 10% of the Sum Insured for Death, Permanent and Total Disablement and Medical Expenses benefits for a flat premium according to the Plan selected by your spouse. | |

| 4 | If I increase or reduce my Sum Insured during the term of cover, will I receive the renewal bonus on the new limit? The first renewal bonus will be calculated at 10% of the revised limit on renewal of the policy and any adjustments under the previous limit will lapse. Renewal bonus applicable to Death and Permanent Total Disablement benefits only. | |

| 5 | Will I be covered if I have to travel and stay out of Singapore? You or any of the Insured Persons are covered for any short term travel out of Singapore up to 6 consecutive months during any period of insurance. The cover for that Insured Person lapses thereafter and all the benefits under the policy for such person shall cease from such date. | |

| 6 | Why are premium rates based on occupation? Each occupation type presents different risk hazards depending on the nature of work and this has a direct effect on the level of premium to be charged. | |

| 7 | I have Personal Accident policies with different insurers. Can I claim from all the insurers if I were to meet with an accident? This will depend on the terms of your policy. Please check with your insurer when in doubt. | |

| 8 | What are the policy exclusions? The key exclusions are war and warlike operations, radioactive and nuclear activity, work on aircraft, dangerous sports, suicide, self-injury, pre-existing physical or mental defect, under influence of drugs (unless prescribed by a registered Medical Practitioner) or alcohol, full time military service, uniformed groups and occupations excluded under the insurance. The full details of the exclusions are contained in the policy. | |

| 9 | How do I make a claim? Please contact our Claims Department as soon as possible after any event giving rise or likely to give rise to a claim and complete a Claim form to facilitate the claim process. Written proof of the accident such as police report, doctor’s report, original medical receipts, invoices and all supporting documents must be furnished as proof of claim. | |

This page is for general information only. The benefits payable are subject to the occurrence of an Accident. You should consider carefully if you intend to switch personal accident policies, which might be detrimental to your current and/or future needs. Full details of the terms, conditions and exclusions of this insurance are provided in the policy and will be sent to you upon acceptance of your application by MSIG Insurance (Singapore) Pte. Ltd.

Ease your helper's transition with the security of our comprehensive maid insurance. Our policy offers mandatory coverage, for both you as employer and your Foreign Domestic Worker (FDW). With benefits like medical expenses, personal accident coverage, hospitalisation and even employer's liability, you can rest assured that you and your helper are well taken care of.

Choose our FDW insurance for unparalleled protection and support for your household and provide your helper with the security they deserve. Trust us to deliver the best in maid insurance solutions.

Up to $60,000 for accidental death and permanent disablement and up to $3,000 for medical expenses such as dental, TCM, and dengue fever.

Up to $120,000 for your maid's hospitalisation and surgical expenses including 90 days pre and post hospitalisation expenses.

Up to $20,000 to send your maid back to her home country following permanent disablement or death.

We will issue a letter of guarantee on your behalf to the Ministry of Manpower (MOM).

Up to $750 to hire a replacement maid if you have to terminate your maid's service due to her injury, illness or death.

Purchase this 26 months’ maid insurance plan directly online and from the comfort of your home.

We keep our process as simple as possible to bring your maid insurance claim to a fair settlement.

| BENEFITS SUMMARY FOR 26 MONTHS | Sum Insured | ||

|---|---|---|---|

| Standard | Classic | Premier | |

SECTION 1Personal accident | |||

| $60,000 per year | $60,000 per year | $60,000 per year |

| $1,000 | $2,000 | $3,000 |

| $500 (sub-limit) | $500 (sub-limit) | $500 (sub-limit) |

| $100 (sub-limit) | $100 (sub-limit) | $100 (sub-limit) |

| $100 (sub-limit) | $100 (sub-limit) | $100 (sub-limit) |

SECTION 2Hospital & surgical expenses | |||

Co-payment conditions as mandated by Ministry of Manpower

Day surgery 90 days pre and post hospitalisation diagnostic services and treatment | $60,000 per policy year | $80,000 per policy year | $120,000 per policy year |

SECTION 3Alternative domestic help | |||

| Pays you for the cost for hiring temporary help when your maid is hospitalised due to an injury or illness | $50 per day (max. 30 days) | $50 per day (max. 45 days) | $50 per day (max. 60 days) |

SECTION 4Wages & levy | |||

| $30 per day (max. 30 days) | $30 per day (max. 45 days) | $30 per day (max. 60 days) |

| $30 per day (max. 14 days) | $30 per day (max. 14 days) | $30 per day (max. 14 days) |

SECTION 5Repatriation expenses | |||

| Pays for the transportation expenses to send your maid back to her home country following permanent disablement or death | $10,000 | $15,000 | $20,000 |

SECTION 6Termination expenses | |||

| Pays for the necessary expenses to terminate your maid’s service if she is certified unfit for work due to injury or illness | $300 | $600 | $600 |

SECTION 7Replacement maid expenses | |||

| Pays the hiring fees for a replacement maid following the termination of your maid’s service due to injury, illness or death. | $500 | $500 | $750 |

SECTION 8Special grant | |||

| Pays a lump sum benefit following death of your maid during her employment in Singapore | $2,000 | $3,000 | $3,000 |

SECTION 9Liability to third parties | |||

| Covers your legal liability for third party accidental bodily injury or property damage as a result of negligence of your maid in the course of and arising out of her employment in Singapore | $5,000 | $10,000 | $20,000 |

SECTION 10Maid’s welfare | |||

| $300 | $300 | $500 |

| $300 | $400 | $500 |

SECTION 11Insurance guarantee bond (to Ministry of Manpower) | |||

| Letter of guarantee for a $5,000 security bond issued on your behalf to the Ministry of Manpower (MOM) | $5,000 | $5,000 | $5,000 |

| BENEFITS SUMMARY FOR 26 MONTHS | Sum Insured |

|---|---|

SECTION 12Waiver of Counter Indemnity for Maid Insurance Guarantee Bond to MOM | |

| Relieves your liability in the event MOM makes a demand for security bond payment (Excess: $250) | - |

SECTION 13Employer’s liability | |

| Covers your legal liability as an employer arising from injury or disease claims by your maid at Common Law | Up to $300,000 |

Up to $500,000 | |

Up to $1,000,000 | |

SECTION 14Reduction of co-payment for Section 2 - Hospital & surgical expenses | |

| Option to reduce the standard 25% co-payment which you have to bear for eligible claims amount above $15,000 | 10% |

0% |

| No. | Questions & Answers | |||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | What is MOM’s enhancement to mandatory medical insurance about? From 1 July 2023, the Ministry of Manpower (MOM) will implement enhancements to the mandatory medical insurance (MI) for all new and existing Work Permits (including Migrant Domestic Workers) and S Pass holders. The MI enhancements are: a) minimum annual hospital and surgical coverage will be increased to $60,000 with a co-payment element for employers for amounts above $15,000. We have enhanced MaidPlus to meet these requirements for policies with period of insurance starting from 1 July 2023. Please visit MOM's website here for more information on the MI enhancements. | |||||||||||||||||||||||||||||||||||||

| 2 | I need a maid insurance policy. How does the MOM’s medical insurance (MI) enhancements affect me? You are required to purchase the maid insurance policy with MOM’s enhanced MI requirements as described under FAQ 1 above. The MaidPlus insurance shown on this page meets these requirements. To apply, you can click here or the “Buy now” button on this page. | |||||||||||||||||||||||||||||||||||||

| 3 | How do I determine the period of insurance start date for my maid policy? The start date is dependent on the type of maid you are hiring:

Based on the required start date, refer to FAQ 2 to apply accordingly. | |||||||||||||||||||||||||||||||||||||

| 4 | My current MaidPlus policy’s period of insurance starts before 1 July 2023. How does the MOM’s latest medical insurance (MI) enhancements affect my existing policy and can I upgrade my policy? Your current MaidPlus insurance policy is not affected by this announcement. You do not need to upgrade your existing policy. Your maid will continue to be covered under the same policy until the current policy expiry date under the policy terms and conditions. We do not offer the option to add MOM’s MI enhancements to your current policy as this is only applicable for policy with period of insurance start date from 1 July 2023. | |||||||||||||||||||||||||||||||||||||

| 5 | What are the key benefit changes to the enhanced MaidPlus starting from 1 July 2023?

| |||||||||||||||||||||||||||||||||||||

| 6 | How does the first $15,000 of cover and 25% co-payment under Section 2 – Hospital & Surgical Expenses (H&S Expenses) work? We will pay for the first $15,000 of the hospital bill. For claim amount above $15,000, the co-payment is 75% by insurer and 25% by the employer up to the covered sum insured under Section 2. Please see the examples below on how these are applied. In the event of a large hospital bill and where the sum insured under Section 2 is depleted, the employer is liable for the remaining hospital bill. Selecting a higher tiered plan can therefore help to reduce your liabilities as illustrated in example 3 compared to example 2. Example 1:

Example 2:

*Employer pays more if the hospital bill exceeds the sum insured under the selected plan. Example 3:

| |||||||||||||||||||||||||||||||||||||

| 7 | How can I reduce my 25% co-payment for hospital bill amount which exceeds $15,000? MaidPlus offers the option to reduce the 25% co-payment to 10% or 0%. This option can be added into any of the three plans. The reduction of co-payment option will help to reduce the cash amount which you have to fork out for hospital bills which is above the first $15,000 up to the sum insured. If you have selected to reduce your co-payment to 0%, you would not be required to pay any cash upfront under example 1 and 3 in FAQ 8. You can select “Reduction of co-payment” option only at the point of purchase and this option cannot be amended once the period of insurance has started. | |||||||||||||||||||||||||||||||||||||

| 8 | Is the first $15,000 cover under Section 2 – Hospital & Surgical Expenses on per hospitalisation or per policy year basis? The first $15,000 cover is on a per policy year basis. It is re-set annually based on the period of insurance start date. Take for example, your maid policy’s period of insurance starts on 1 January. In February, your maid was admitted to the hospital for injury and incurred a bill of $15,000. We pay the entire bill as it falls within the first $15,000. In November of the same year, your maid was once again admitted to hospital for another injury and incurred a bill of $10,000. The co-payment would apply immediately for the second bill where we would pay 75% ($7,500) and employer would pay 25% ($2,500). On 1st January of the following year, the first $15,000 cover will re-set and we will pay the first $15,000 for any new hospital bills incurred in the new policy year. | |||||||||||||||||||||||||||||||||||||

| No. | Questions & Answers | |

|---|---|---|

| 9 | What is the difference between Section 1 – Personal Accident Medical Expenses and Section 2 – Hospital & Surgical Expenses benefits? Section 1 – Personal Accident Medical Expenses cover outpatient medical expenses such as the cost of dental treatment, Traditional Chinese Medicine (TCM) treatment due to injury and treatment for dengue fever. Section 2 - Hospital & Surgical Expenses cover for inpatient treatment at a hospital as a result of major illnesses or accidents. In addition, medical expenses incurred during the 90 days’ pre and post-hospitalisation as well as day surgery are covered. | |

| 10 | How does the Wages & Levy benefit work? MaidPlus will reimburse you for your helper’s wages and levy for the period: a) she is hospitalised due to an injury or illness for up to 60 days and where Section 2 is payable. | |

| 11 | How does the Alternative Domestic Help benefit work? This benefit relieves an employer by reimbursing a fixed daily sum of $50 up to 60 days, to supplement the cost of hiring alternative domestic help if your maid is hospitalised due to a covered injury or illness. | |

| 12 | Will my maid be covered when she travels back to her country for home leave? When your maid goes on home leave, she will be covered only for the Accidental Death and Permanent Disablement benefit, provided her work permit is not cancelled during the travel period. All other benefits under the plan will temporarily cease until she returns to work in Singapore. | |

| 13 | Will my maid be covered if she is hospitalised during an overseas holiday trip? Do I need to buy travel insurance for her? MaidPlus will cover hospitalisation expenses incurred during an overseas trip due to injury or illness sustained by your maid outside Singapore, provided she is travelling with you. However, we recommend purchasing a separate travel insurance for your maid as the travel benefits provided are more relevant and comprehensive to deal with overseas situations where medical and evacuation costs incurred are much higher. Please refer to MSIG TravelEasy for more details. | |

| 14 | Does MaidPlus pay for COVID-19 related medical bills? MaidPlus covers for inpatient treatment for COVID-19. | |

| No. | Questions & Answers | |

|---|---|---|

| 15 | Are pre-existing conditions covered? Pre-existing conditions are covered after the maid’s first 12 months of employment with the same employer. However, this does not include birth defects, congenital abnormalities, hereditary conditions and their associated conditions. | |

| 16 | Will my helper’s pre-existing medical condition be covered when I apply for MaidPlus which includes MOM’s latest enhancements or if I upgrade her to a higher MaidPlus plan during the renewal of her work permit? Hospital and surgical expenses for pre-existing condition is covered after your maid’s first 12 months of employment with you. This is subject to the following limits under Section 2 – Hospital & Surgical Expenses, applicable to all plans: a) Sum insured up to $60,000 and The above is subject to policy terms and condition such as permanent exclusion for birth defects, congenital abnormalities, hereditary conditions and their associated conditions. | |

| No. | Questions & Answers | |

|---|---|---|

| 17 | How does the Maid Insurance Guarantee Bond and waiver of counter indemnity work? We will issue a Letter of Guarantee for a $5,000 security bond on your behalf to MOM. If MOM makes a demand, we will first make the payment and recover the payment from you under the policy conditions of the section on the Maid Insurance Guarantee Bond. You can purchase the optional cover for Waiver of Counter Indemnity to reduce your liability to re-pay us for the bond payment to $250. | |

| 18 | When will the Maid Insurance Guarantee Bond record be received by MOM? For new and transfer maid policies which are purchased:

For renewal maid policy:

| |

| 19 | Do I need to buy the Philippine Overseas Labour Office (POLO) Bond for my Filipino maid when she goes back to the Philippines for home leave? With effect from 8 September 2022, the POLO Bond is no longer required by the Philippine Overseas Labour Office. | |

| No. | Questions & Answers | |

|---|---|---|

| 20 | How will I receive my maid insurance policy? We will send your MaidPlus policy to the email address you have provided in the application after successful payment for online application submitted here. Please check your junk or spam mail if you do not see it in your inbox. | |

| 21 | Do I get a refund if I cancel my MaidPlus insurance policy? You can cancel the policy by emailing us a written instruction or through your intermediary. We will cancel the policy provided full discharge is given to us in writing by MOM in respect of our liability under Section 11. You will receive a refund of the premium based on our short-period rates for the unexpired period of insurance coverage, subject to a minimum charge of $50 as stated in the cancellation conditions of the policy. There will be no refund if the cancellation is made 180 days or more after the commencement date of the period of insurance or if there is any claim made on the policy. | |

| 22 | Can I change my plan once the policy has started? Mid-term change of plans is not allowed once the cover has commenced. Therefore, to ensure you and your helper are adequately protected, please select the plan that best fits your needs at the start of the cover. | |

| 23 | Why is the maid insurance covering 26 months instead of 24 months? MOM requires the extra two months of maid insurance to ensure that even after the maid's work permit expires, there is insurance coverage for your maid while they are in Singapore and when repatriation is not immediate. | |

| 24 | How do I make a claim? Please contact our Claims Department as soon as possible after any event giving rise or likely to give rise to a claim and complete a Claim form to facilitate the claim process. Written proof of the accident, such as a police report, doctor's report, original medical receipts, invoices and all supporting documents, must be furnished as proof of claim. For medical expenses claims arising from hospital admission, we will assess your claims submission and notify you of the outcome. Thereafter, we will make direct payment to the hospital for our share of the hospital expenses if it is an admissible claim. | |

From 1 July 2023, the Ministry of Manpower (MOM) will implement enhancements to the mandatory medical insurance (MI) for all new and existing Work Permits (including Migrant Domestic Workers) and S Pass holders.

The MaidPlus product shown on this page has been enhanced to meet the MOM’s latest MI requirements.

Please refer to the FAQs above for more information.

MaidPlus pre-contract disclosure

(Applicable for policies with period of insurance start date from 1 July 2023)

MSIG’s MaidPlus provides coverage for the following features that comply with the Ministry of Manpower’s (MOM) enhanced Medical Insurance requirements.

Please refer to the FAQs above for more information.

This page is for general information only. Full details of the terms, conditions and exclusions of this insurance are provided in the policy and will be sent to you upon acceptance of your application by MSIG Insurance (Singapore) Pte Ltd.

This policy is protected under the Policy Owners’ Protection Scheme which is administered by the Singapore Deposit Insurance Corporation (SDIC). Coverage for your policy is automatic and no further action is required from you. For more information on the types of benefits that are covered under the scheme as well as the limits of coverage, where applicable, please contact us here or visit GIA / LIA or SDIC.

12 Aug 2025

The following article was published in Asia Insurance Review on 1 August 2025.

To MSIG Singapore’s Mr Jeremy Lian, it is first important to understand the scope of what cyber insurance is designed to cover. Second, he said it is crucial to maintain a clear and detailed timeline of a cyber incident from the moment it is detected, as it could make a difference in ensuring a smooth and timely claims process.

By Sarah Si

In Singapore, cyber insurance policies tend to come with some exclusions and limitations that policyholders should be aware of, according to MSIG Singapore senior vice president (technical services) Jeremy Lian.

“To begin with, it is important to understand the scope of what cyber insurance is designed to cover. These policies typically focus on intangible losses such as data breaches, business interruption and reputational harm,” said Mr Lian, speaking to Asia Insurance Review.

“They do not extend to physical property damage or personal injury, which are covered under other lines of insurance.”

He also said most cyber insurance policies exclude coverage for war and state-sponsored cyberattacks due to the systemic risks and attribution challenges involved.

Deductibles across the cyber insurance market remain high as well, Mr Lian pointed out, saying, “This reflects the significant expenses involved in incident response ranging from forensic investigations and legal counsel to crisis communications.”

He also made sure to highlight that as insurance “is designed to mitigate part of the financial impact following an incident”, policyholders should still invest in strengthening their own cyber defences.

Even when coverage is triggered in the case of an event, he noted insurers may face restrictions on how certain claims are handled, as well.

Citing ransom payments as an example, he said they were subject to “tight regulatory constraints” such as anti-money laundering laws and sanctions regimes. These restrictions mean insurers may not be able to reimburse ransom payments if there is a risk the funds could end up with a sanctioned entity or be linked to terrorist financing, he said.

“Another area where coverage is tightening is social engineering. As impersonation scams and business email compromise become more sophisticated, insurers may cap limits or narrow the terms for these types of claims,” he said.

“These incidents are difficult to verify and prevent, making them a growing concern for underwriters.”

He pointed out that insurers are now prioritising “the strength of an organisation’s cyber security posture”, as well.

He said, “Companies with poor security controls may face more restrictive terms or may not be able to secure cover. On the other hand, organisations that demonstrate maturity in their cyber risk management are more likely to secure broader protection and more favourable terms.”

Taken together, these exclusions and limitations highlight the growing importance of cyber governance, he noted.

According to Mr Lian, his company works closely with third-party service providers and InsurTechs with AI capabilities to support them when it comes to improving cyber offerings.

He noted that this includes enhancing threat detection, to streamlining the insurance application process, automating assessment and generating data-driven evaluations of applicants’ cyber exposures.

“This collective approach allows us to employ advanced technologies more effectively across the value chain and continuously improve our cyber offering,” he said.

In the event of a cyberattack, “particularly in urgent scenarios like ransomware, having the right documentation can make a significant difference in ensuring a smooth and timely claims process”, according to Mr Lian.

He said, “While some cyber insurance policies offer 24/7 access to incident response support, the effectiveness of the claims process often depends on how well the incident is documented by the policyholder.”

As a result, he noted that it is considered best practice for organisations to maintain a clear and detailed timeline of the incident from the moment it is detected.

“This includes recording all actions taken to contain and recover from the attack, preserving forensic reports and keeping a record of all communications related to the incident be it with the attackers, internal teams or external stakeholders,” he said.

To substantiate financial losses, he noted that companies should be prepared to share supporting documentation such as calculations of their lost revenue and additional operating expenses. In addition, he said reports filed with law enforcement or regulatory authorities should also be included.

He said, “All of this would build a detailed picture to quickly resolve the immediate emergency with regards to your computer system and allow swift resolution on matters with regards to financial and third-party indemnity.”

When asked if the current regulatory environment in Singapore was supportive for cyber policies, Mr Lian noted that it was broadly so, of the growth of coverage. He also said the country engenders a multi-agency approach by authorities such as the Infocomm Media Development Authority (IMDA) and Monetary Authority of Singapore (MAS), which “tackle the different challenges for each respective sector”.

In particular, he pointed out that MAS has established the Cyber and Technology Resilience Experts (CTREX) Panel, which comprises of global industry thought leaders, experts and practitioners in cyber security and technology resilience.

“This panel advises on emerging risks and has put forth recommendations that are already shaping how financial institutions approach cyber resilience,” he said.

“These include adopting a service-centric view of operational resilience, addressing third-party and open-source software risks, preparing for post-quantum cryptography and enhancing anti-scam measures through AI-driven fraud detection and phishing-resistant authentication.”

He also cited the Model AI Governance Framework for generative AI, launched by introduced by IMDA to set new benchmarks for responsible AI use, as an example. Saying it complemented developments such as the CTREX Panel, Mr Lian highlighted that as AI-related risks become more prominent in underwriting and claims, such frameworks are increasingly relevant to cyber insurers looking to stay ahead of emerging threats.

“These regulatory efforts have not only improved cyber hygiene across industries but also fostered stronger public-private collaboration and heightened awareness of systemic cyber risks and the need for cyber insurance,” he said.

With the pace and complexity of cybercrimes accelerating, Mr Lian pointed out that it is becoming more difficult for insurers to anticipate how the threat landscape will evolve. He said, “This challenge is compounded by limited claims data on emerging technologies, making it harder to assess risk accurately and price coverage appropriately.”

As a result, he highlighted that many cyber policies are playing what he called “a reactive game of catch-up”, and cited industry kneejerk reactions to exclude widespread events like Log4j and Solarwinds.

“Such reactions, although necessary to mitigate catastrophic losses, often are disruptive and does generate negative sentiments to the adoption of cyber insurance,” he said.

To stay ahead, he suggested insurers consider other methods to mitigate such issues, such as adopting a more agile, data-informed review as often as possible and collaborating closely with the cyber security industry, reinsurers and public bodies to close the gap as regulatory expectations and threat vectors continue to evolve.

Mr Lian expects ransomware to remain a major concern over the coming year.

“Threat actors could evolve their tactics, and with GenAI in the mix, they are now able to launch more sophisticated, multi-stage attacks,” he said.

“The use of Gen AI is also making social engineering easier to scale and vulnerabilities quicker to exploit.”

At the same time, he believes supply chain attacks becoming more mainstream will push insurers to rethink how they assess ecosystem risk and drive a demand for policies that can better address third-party exposures, not just direct ones.

“What will be interesting is how the industry will be shifting, with a stronger push to embed risk mitigation into the insurance offering itself,” he said.

“Value-added services like employee training and incident response support will become essential, rather than add-ons, in helping clients to stay insurable in a much more complex threat environment.”

Lastly, he forecast more joint efforts between the public and private sectors to tighten cyber defences.

He said, “As AI becomes more embedded in how we operate, there is going to be a real focus on using it responsibly, with the right data controls and governance in place to avoid legal and ethical pitfalls.”

Discover the flexibility of MSIG's home insurance plans, designed to adapt to your unique home needs. Whether you live in a cosy apartment or a spacious residence, our home insurance solutions can be tailored to provide the perfect level of protection. Customize your coverage to include everything from personal liability to protection for home contents, renovations, and special possessions.

With MSIG, you have the freedom to choose the coverage that best suits your lifestyle. Our adaptable policies ensure you only pay for what you need, and the reassurance that there are no unnecessary costs . Trust MSIG for the fine home insurance protection you are looking for.

Customise your coverage to cover your special possessions or sum insured you prefer.

Wherever you may be, we protect you with free personal liability cover of up to $1 million.

Protect your valuables and personal possessions for a total peace of mind.

Cover extends to accidental breakage of mirrors/glass, frozen food spoilage, monthly service and conservancy fees and fraud by your domestic helpers.

Our plan takes care of your temporary accommodation cost, emergency cash, conservancy charges, and even loss of rent.

Save time by submitting your property or liability insurance claim online! We keep our process as simple as possible to bring your claim to a fair settlement.

| BENEFITS SUMMARY | Sum Insured |

|---|---|

SECTION 1Home Contents | |

| Home Contents* ^ + Household furniture and furnishings, including personal belongings. Valuables covered up to 1/3 of Sum Insured, subject to single article limit at 5% of Sum Insured | Sum as proposed by Insured |

| Contents temporarily removed up to 30 days but within Singapore* | 15% of the Sum Insured on Home Contents |

| Replacement of locks and keys* | $250 |

| The accidental death of you and your spouse in your home caused by fire or thieves | $15,000 or half of the Sum Insured on Home Contents whichever is lesser and in the aggregate |

| Alternative accommodation or loss of rent | 10% of the Sum Insured on Home Contents |

| Deterioration of frozen foods due to failure of your freezer* | $500 |

| Worldwide cover for a stolen credit card or loss of personal money* | $1,000 |

| Domestic servant’s belongings* | $500 |

| Removal of debris* | $10,000 |

| The accidental death of pedigree pets* | $500 |

SECTION 2Special Possessions (Optional) | |

| Unspecified personal possessions and valuables*^++ | Sum as proposed by Insured, subject to $2,500 any one article |

| Specified personal possessions and valuables*^++ | Sum as proposed by Insured |

SECTION 3Personal Liability (Free with Home Contents and/or Buildings cover) | |

| Worldwide personal legal liability for you and your family | $1,000,000 |

| Liability as a tenant* | $500,000 |

SECTION 4Buildings | |

| Buildings including fixtures and fittings* | Sum as proposed by Insured |

| Professional fees, debris removal and additional cost of complying with Statutory Building Regulations* | Up to the Sum Insured on Buildings |

| Alternative accommodation or loss of rent* | 15% of the Sum Insured on Buildings (max $50,000) |

| Fire extinguishing expenses* | $2,500 or the amount of expenses, whichever is lower |

Note: Section 1 and/or 4 must be purchased first. Section 2 is optional.

*Excess of $100 for each and every claim.

^If any article forms part of a pair or set suite, group or collection, colour, pattern or design, we will pay only for the value of the article and not for any higher value the article may have as part of a pair or set suite, group or collection, colour, pattern or design.

+Excludes contact lenses, handphones and pagers.

++Excludes money, credit cards, contact lenses, handphones, pagers and portable computers.

| No. | Questions & Answers | |

|---|---|---|

| 1 | If I have a HDB fire policy or Fire Mortgage insurance with my bank, do I need to buy separate Home Insurance coverage? The cover effected under the HDB fire policy or your Mortgage Fire insurance usually relates to the building structures, permanent fixtures and fittings only. Your home contents and personal belongings may not be covered. Home Insurance provides this cover plus the option to cover your personal possessions. | |

| 2 | What is the definition of "Buildings"? "Buildings" refers to the structure of your private residence including: outbuildings used for domestic purposes, decorative finishes, swimming pools, tennis hard courts, garden walls, patios, terraces, hedges, fences, gates, paths and drives | |

| 3 | What is the definition of "Home Contents"? "Home Contents" refers to household items of furniture, furnishings, home appliances, personal computers, books, toys, clothing and other movable personal belongings including valuables. | |

| 4 | How much should I insure for Buildings and Home Contents? For Buildings, the sum to be insured should be the cost of rebuilding the buildings at the time of the loss or damage. For Home Contents, the sum to be insured should reflect the cost of replacing the insured property to its original condition (or its equivalent) at the time just before the damage. If the Sum Insured for Building and Home Contents is inadequate, claims payment will be made after the deduction for any wear and tear or depreciation. | |

| 5 | What is accidental loss or damage? This refers to loss or damage caused by fire, theft, flood and any accidental cause so long as it is not excluded under this insurance. | |

| 6 | What are "Valuables"? "Valuables" are jewellery, watches, furs, curios, works of art, antiques, stamps and coin collections and other collectable property, manuscripts, medals, items of gold, silver or other precious metals or precious stones. | |

| 7 | Are the personal belongings of my domestic maid covered under Home Insurance? The Home Contents section provides cover of up to $500 for personal effects such as clothing and personal items belonging to your domestic maid who is permanently living with you. | |

| 8 | How do I make a claim? Please contact our Claims Department as soon as possible after any event giving rise or likely to give rise to a claim and complete a Claim form to facilitate the claim process. Written proof of the accident such as police report, invoices and all supporting documents must be furnished as proof of claim. | |

This page is for general information only. Full details of the terms, conditions and exclusions of this insurance are provided in the policy and will be sent to you upon acceptance of your application by MSIG Insurance (Singapore) Pte Ltd.

This policy is protected under the Policy Owners’ Protection Scheme which is administered by the Singapore Deposit Insurance Corporation (SDIC). Coverage for your policy is automatic and no further action is required from you. For more information on the types of benefits that are covered under the scheme as well as the limits of coverage, where applicable, please contact us here or visit GIA or SDIC.

| Home Insurance | HomeEasy | Enhanced HomePlus | |

|---|---|---|---|

Suitable for | All property types including landed properties owners, landlords and tenants | HDB and private apartment owners, landlords and tenants | All property types including landed properties owners, landlords and tenants |

Coverage | All risks cover Sum insured as proposed | Insured perils only Choose from 2 plans with 3 optional benefits | Insured perils only Choose from 3 plans with 2 optional benefits |

Home Contents | Sum imsured as proposed | Up to $80,000 | Up to $120,000 with option to increase sum insured* |

Renovations | As per sum insured under building section | Up to $120,000 | Up to $150,000 with option to increase sum insured* |

Energy efficient appliance upgrade | Not Available | 10% in addition | Not Available |

Emergency home assist | Not included | Included | Included |

Personal cyber | Not Covered | Covered | Not Covered |

Personal Legal LiabilityTenant liabilityProperty owner's liability | $1,000,000 $500,000 $1,000,000** $1,000,000 in aggregate | $1,000,000 $500,000 $500,000 $1,000,000 in aggregate | $1,000,000 $500,000 $1,000,000** $1,000,000 in aggregate |

Building | Available as optional cover Sum insured as proposed | Not Available | Available as optional cover Sum insured as proposed |

Special possessions | Available as optional cover Sum insured as proposed | Not Available | Not Available |

Family accidental death protection | Not Available | Available as optional cover | Covered |

Bicycle and mobility scooter locked outside your home | Not Available | Available as optional cover | Not Available |

Worldwide cover for personal effects | Not Available | Available as optional cover | Not Available |

Coverage duration | 1 year | 1 year, 3 year and 5 year | 1 year |

* For Ultimate plan only

** Applicable when Building cover is purchase

08 Dec 2025

Complimentary plan offers up to $100 in accident coverage and affordable upgrades from just $0.20 per day

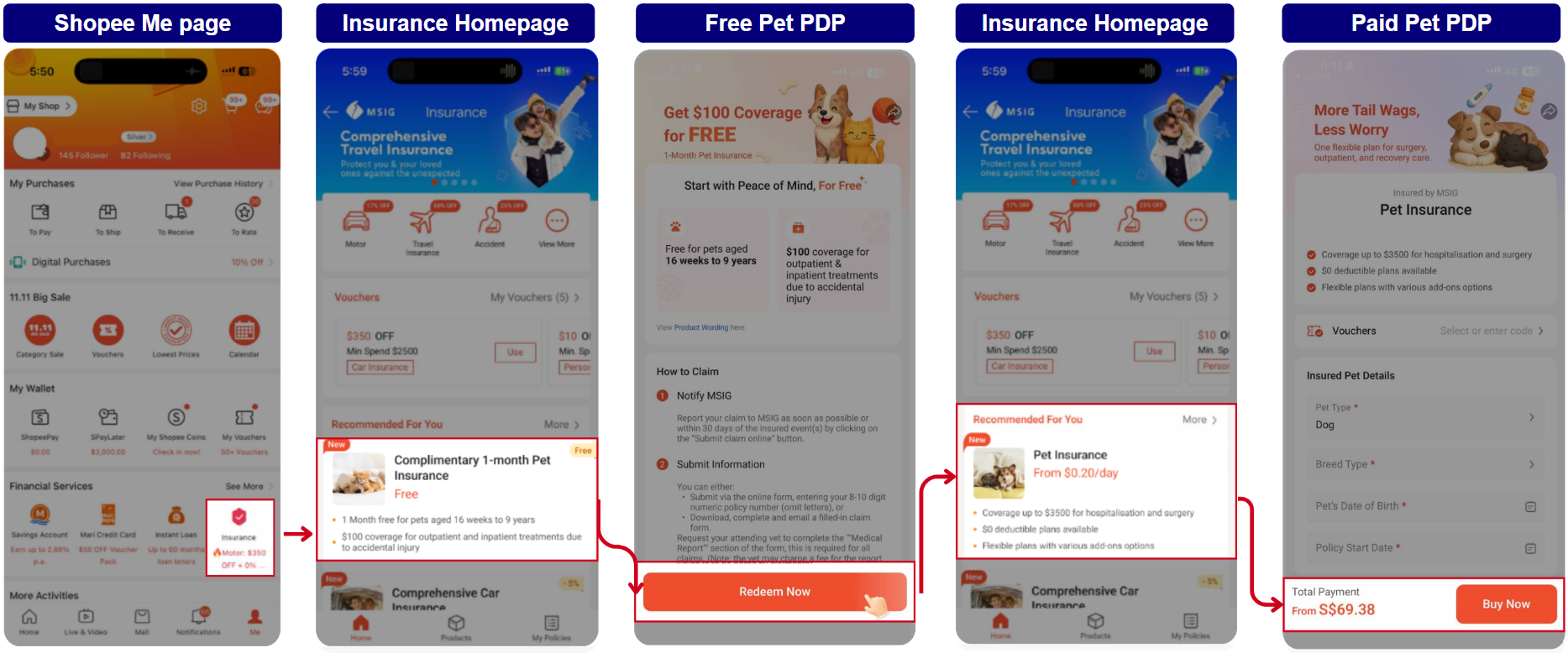

Monee, a leading digital financial services provider in Southeast Asia with a growing presence in Latin America, has partnered with general insurer, MSIG Insurance, to launch a new Pet Insurance product designed to provide pet owners with enhanced financial security and peace of mind while caring for their beloved animal companions.

In conjunction with this launch, a Free One-Month Pet Insurance* is now available to pet owners, which provides a complimentary coverage of up to $100 for outpatient and inpatient treatment resulting from accidental injury. This initiative aims to raise awareness of the importance of pet protection while easing some financial costs for pet owners.

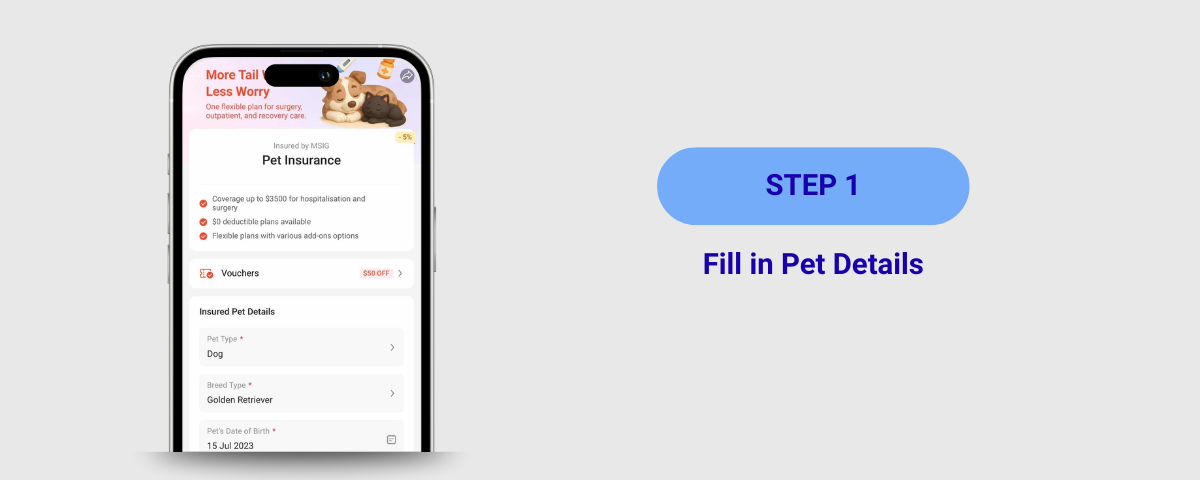

For owners seeking extensive coverage, MSIG offers affordable plans starting from just $0.20/day, with key benefits that include:

“As a pet owner, I understand how stressful it can be when pets need unexpected medical care,” said Yang Yang, Regional Director, Monee Insurance. “Our goal at Monee is to make insurance simple and affordable so every pet has access to the care they deserve - starting with free protection and flexible upgrades from just $0.20 a day.”

Steven Leong, Head of Retail Distribution, MSIG Singapore added, “Our partnership with Monee reinforces our shared commitment in making insurance accessible and part of everyday life. Building on the success of our travel, car and personal accident insurance offerings which are already available on Shopee, we are excited to continue delivering innovative and value-driven solutions, to protect the goals and aspirations of our customers.”

For more information and media enquiries, please contact:

Carole Chow

AVP, Brand & Communications

MSIG Insurance (Singapore) Pte. Ltd.

D: +65 6012 1258

In conjunction with the launch and the upcoming 12.12 Shopee Birthday Sale, Monee is offering pet owners up to 24% off on plan upgrades, with prices starting from just $0.20/day.

Click here or follow the steps below to redeem your Free 1-month pet insurance. For full coverage, click here to purchase your Comprehensive pet insurance today!

Note: Pet Insurance is underwritten by MSIG Insurance (Singapore) Pte Ltd and distributed by MoneeInsure Agency SG Private Limited (“MoneeInsure Agency”). The Shopee Singapore platform is solely a marketplace. The Insurance page on the Shopee platform is owned and operated by MoneeInsure Agency. All insurance products displayed on the Shopee Singapore platform are solicited, arranged and administered by MoneeInsure Agency SG Private Limited.

For redemption/purchasing instructions, please see Annex A for a step-by-step guide.

* Terms and Conditions apply.

Annex A:

Free 1-month Pet Insurance

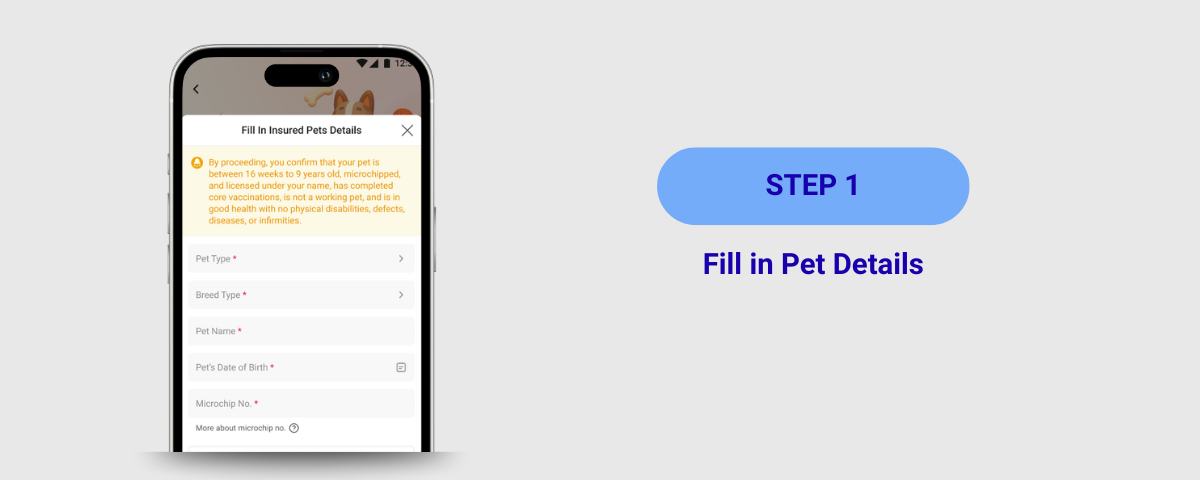

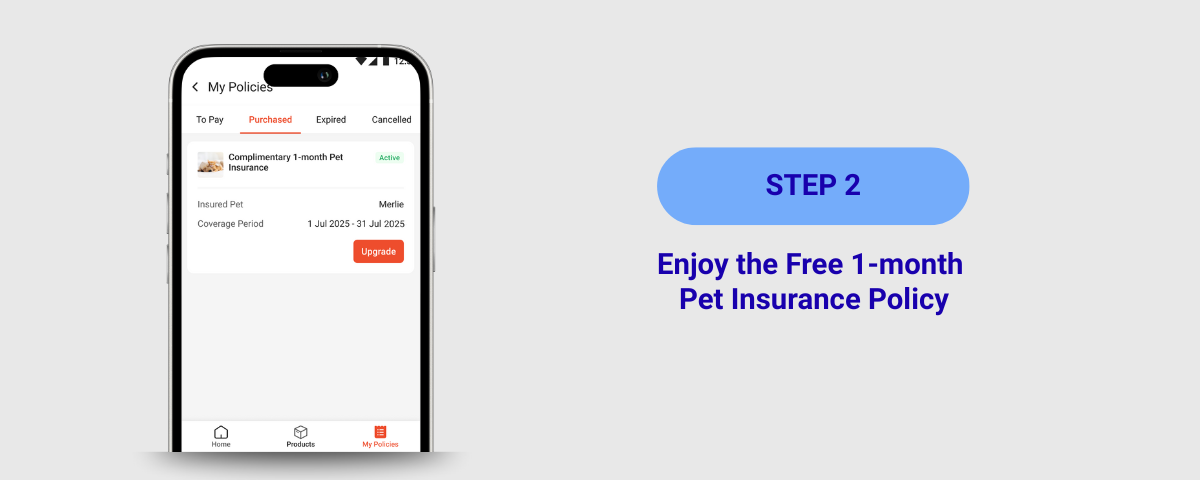

Claim a free 1-month policy within 5 mins:

Pet Insurance

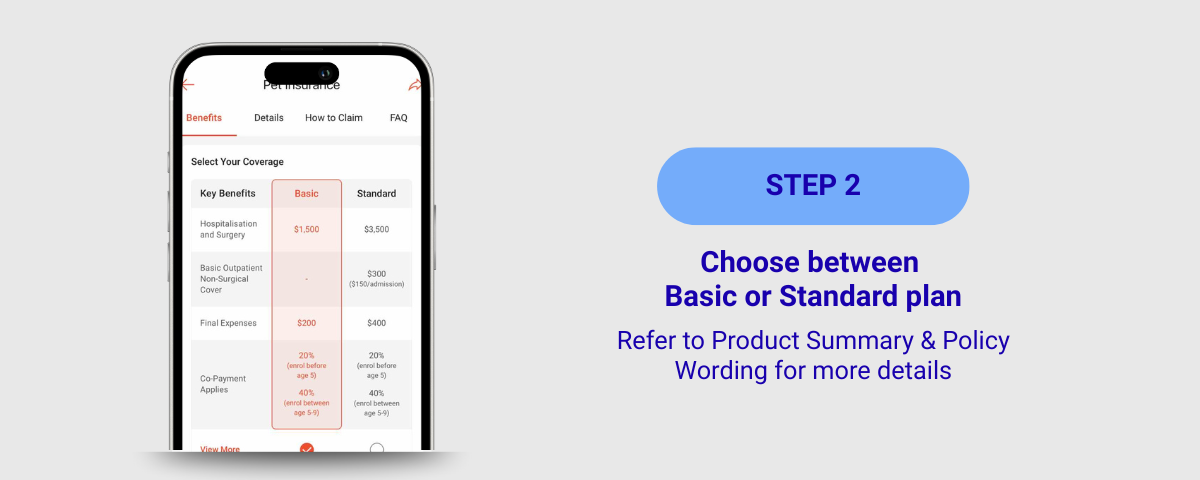

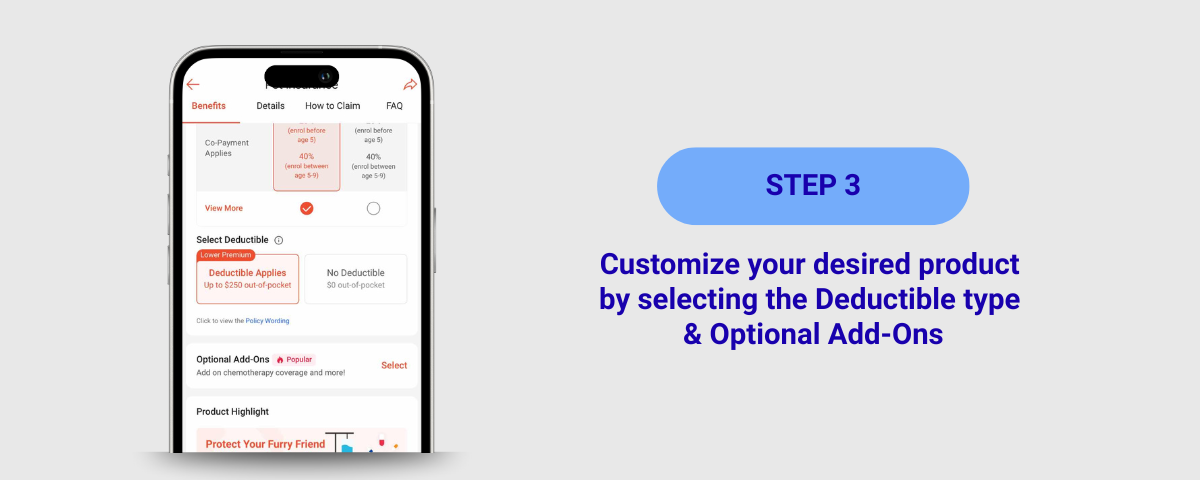

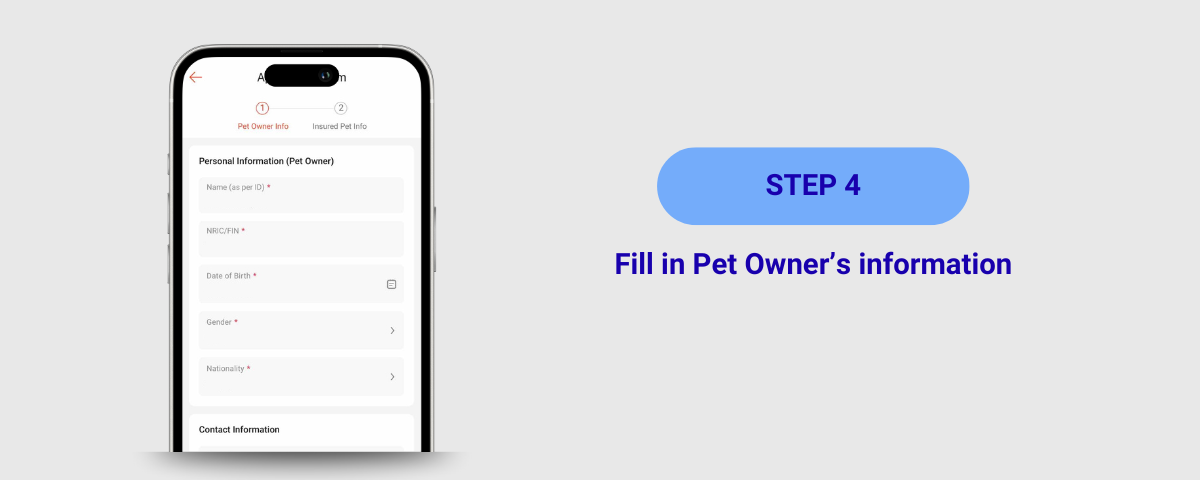

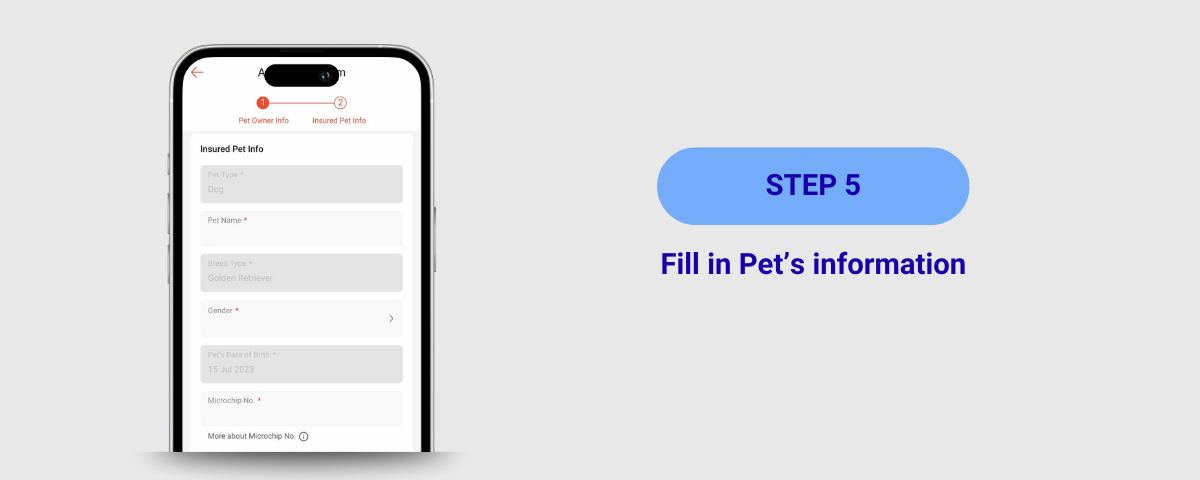

Featuring an easy and seamless 6-step purchase journey:

Monee is a leading digital payments and financial services provider in Southeast Asia, with a growing presence in Latin America. Its mission is to better the lives of individuals and businesses in the region with financial services through technology.

Monee delivers a comprehensive range of digital financial products and services, including mobile wallets, payment processing, credit, banking, and insurtech. By leveraging technology and strategic partnerships, Monee aims to drive greater digital financial inclusion, convenience, and accessibility for individuals and small businesses across Southeast Asia and Latin America.

Monee is part of Sea Limited, a leading global consumer internet company. To learn more, visit www.monee.com.

A leading general insurer with a local presence of over 100 years, MSIG Singapore offers an extensive range of insurance solutions for commercial and personal risk protection, enabling the security and safety of individuals and businesses. MSIG Singapore holds an A+/Stable financial rating by Standard & Poor's.

MSIG Singapore has garnered numerous awards for delivering digitally innovative and customer-centric solutions. The company was named ‘Best General Insurer for Singapore’ by InsuranceAsia News and was awarded ‘Personal Lines Insurer of the Year’ and ‘Underwriting Excellence’ by Re(in) Asia.

MSIG is a subsidiary of Mitsui Sumitomo Insurance Co., Ltd, and a member of the MS&AD Insurance Group – one of the largest general insurance groups in the world with presence in 50 countries and regions globally, 18 of which are in Asia Pacific including all ASEAN markets as well as in Australia, New Zealand, China, Hong Kong, Taiwan, South Korea and India. Headquartered in Japan, MS&AD is amongst the top non-life insurance groups in the world based on gross revenue.

10 Mar 2025

It was to be a much-anticipated holiday to Guangzhou for our policyholder and her 17-year-old son. As a preschool teacher who was in excellent health, our policyholder had every reason to expect a joyful trip. However, their adventure took a sudden and alarming turn when she experienced severe symptoms and was rushed to the hospital. There, our policyholder was diagnosed with a critical aortic dissection, a life-threatening condition that required an urgent open-heart surgery.

Her husband, upon receiving the distressing news, immediately sought help from MSIG. With their son being a minor and unable to provide consent, the husband flew to Guangzhou to be by his wife's side. The hospital required a RMB 200,000 (S$40,000) deposit before proceeding with the surgery.

Our emergency travel provider promptly issued a guarantee for medical expenses, enabling the successful operation. As our policyholder gradually showed signs of improvement, we arranged for repatriation with a nurse escort for her safe return to Singapore. Plans were made swiftly for her return flight, and we successfully transferred her to a local hospital in Singapore for continued care.

Reflecting on the ordeal, her husband, Charlie expressed deep gratitude for the unwavering support they received.

Imagine driving on the expressway, minding your own business, when suddenly another car collides with yours, sending you crashing into the centre divider.

This was the unfortunate reality for one of our insured drivers, part of a commercial fleet we cover for a client. Thankfully, our insured driver was not seriously injured, but the car was a total loss, beyond economical repair.

Despite clear evidence, the third-party insurer denied liability due to their policyholder's non-cooperation.

Faced with the challenge of a third-party motorist with no apparent business interests, the odds of recovering our losses seemed slim. But we didn't give up. MSIG’s claims team conducted a thorough background check and discovered that the motorist owned and inherited a landed property.

After more than five years of relentless persistence, the third-party finally agreed to sell his estate to repay the subrogation claim and cover legal costs.

Kamini Kanagalingam

Senior Vice President, Claims Services

Introducing TravelEasy Flex, the ultimate travel insurance plan that adapts to your unique needs. With flexible options, you can customize your coverage to include only what you need, ensuring you get the best value. Enjoy peace of mind with benefits like Cancel-For-Any-Reason (CFAR) coverage up to $6,000, compensation for every 4-hour of travel delay, and special group discounts, including child rates.

Choose TravelEasy Flex for comprehensive, affordable travel insurance with unparalleled flexibility and protection. Travel confidently, knowing you're covered by the best in the industry. Buy today and embark on a worry-free journey!

Get up to $2,400 for travel delays. Benefit payable from just 4 hours of delay. Now, that’s shorter than most other plans!

Enjoy up to 10% discount on group cover, including child premiums. Include your extended family, friends, and even your domestic helper under one policy!

Up to $6,000 for travel, accommodation and entertainment expenses if you must cancel your trip. Buy within 14 days of trip booking to qualify.

Extend your policy to cover adventurous activities and sports equipment. Or choose Golfer’s cover for up to $2,300 protection on golf equipment and more.

Up to $350,000 for overseas inpatient medical expenses and emergency evacuation due to acute onset of pre-existing medical conditions.

Insure up to $2,600 for self-driving trips, covering rental vehicle cancellation, damage excess, and return due to sickness or injury.

Getting single or annual travel insurance has never been easier! Buy online and receive your e-policy instantly!

Our travel emergency hotline and live chat ensure there is always someone to connect you to medical care and evacuation, no matter which time zone you are in.

Save time by submitting your travel insurance claim online! We keep our process as simple as possible to bring your claim to a fair settlement.

| Base cover benefits | Sum insured per trip | ||

|---|---|---|---|

| Standard Flex Plan | Elite Flex Plan | Premier Flex Plan | |

Personal accident cover | |||

Section 1Personal accident | |||

| Adult below 70 years | $200,000 | $300,000 | $500,000 |

| Adult 70 years & above | $40,000 | $60,000 | $80,000 |

| Child | $70,000 | $100,000 | $120,000 |

| Family | $540,000 | $800,000 | $1,240,000 |

| Base cover benefits | Sum insured per trip | ||

|---|---|---|---|

| Standard Flex Plan | Elite Flex Plan | Premier Flex Plan | |

Section 14Insolvency of licensed travel operator | |||

| Adult / Child | $2,000 | $4,000 | $6,000 |

| Family | $5,000 | $10,000 | $15,000 |

Section 15Travel cancellation | |||

| Adult / Child | $8,000 | $10,000 | $15,000 |

| Family | $20,000 | $25,000 | $37,500 |

Section 16Travel postponement | |||

| Adult / Child | $600 | $1,200 | $1,800 |

| Family | $1,500 | $3,000 | $4,500 |

Section 17Replacement of Traveller | |||

| Adult / Child | $500 | $750 | $1,000 |

| Family | $1,250 | $1,875 | $2,500 |

Section 18Unused entertainment ticket | |||

| Adult / Child | $100 | $300 | $500 |

| Family | $250 | $750 | $1,250 |

Section 19Delayed departure | |||

| Adult | $360 $60 every 4 hrs | $600 $60 every 4 hrs | $1,200 $60 every 4 hrs |

| Child | $180 $30 every 4 hrs | $300 $30 every 4 hrs | $600 $30 every 4 hrs |

| Family | $720 | $1,200 | $2,400 |

Section 20Flight diversion | |||

| Adult | $500 $100 every 6 hrs | $1,000 $100 every 6 hrs | $1,500 $100 every 6 hrs |

| Child | $250 $50 every 6 hrs | $500 $50 every 6 hrs | $750 $50 every 6 hrs |

| Family | $1,000 | $2,000 | $3,000 |

Section 21Overbooked flight | |||

| Adult / Child | $200 $100 every 6 hrs | $300 $100 every 6 hrs | $400 $100 every 6 hrs |

| Family | $400 | $600 | $800 |

Section 22Missed travel connection | |||

| Adult / Child | $400 $100 every 6 hrs | $500 $100 every 6 hrs | $600 $100 every 6 hrs |

| Family | $800 | $1,000 | $1,200 |

Section 23Shortening the trip | |||

| Adult / Child | $5,000 | $10,000 | $15,000 |

| Family | $12,500 | $25,000 | $37,500 |

Section 24Travel disruption | |||

| Adult / Child | $1,000 $200 per room per night | $2,000 $300 per room per night | $3,000 $400 per room per night |

| Family | $2,500 | $5,000 | $7,500 |

Section 25Automatic extension of cover | Covered | Covered | Covered |

Section 26Delayed baggage | |||

| Adult / Child | Overseas: $300 $100 every 6 hrs Delay in Singapore: $100 after 6 hrs | Overseas: $600 $150 every 6 hrs Delay in Singapore: $150 after 6 hrs | Overseas: $1,000 $200 every 6 hrs Delay in Singapore: $200 after 6 hrs |

| Family | $600 | $1,200 | $2,000 |

Section 27BaggageSub-limit: $500 per article, pair or set of items and $1,000 for one unit laptop computer | |||

| Adult / Child | $3,000 | $5,000 | $7,500 |

| Family | $6,000 | $10,000 | $15,000 |

Section 28Loss of travel documents | |||

| Adult / Child | $500 | $1,000 | $1,500 |

| Family | $1,000 | $2,000 | $3,000 |

Section 29Personal money | |||

| Adult / Child | $100 | $300 | $500 |

| Family | $200 | $600 | $1,000 |

| Base cover benefits | Sum insured per trip | ||

|---|---|---|---|

| Standard Flex Plan | Elite Flex Plan | Premier Flex Plan | |

Section 30Personal liability | |||

| Adult | $600,000 | $800,000 | $1,000,000 |

| Child | $300,000 | $400,000 | $500,000 |

| Family | $600,000 | $800,000 | $1,000,000 |

| Base cover benefits | Sum insured per trip | ||

|---|---|---|---|

| Standard Flex Plan | Elite Flex Plan | Premier Flex Plan | |

Section 31Terrorism cover | |||

| Adult / Child | $200,000 | $300,000 | $500,000 |

| Family | $800,000 | $1,200,000 | $2,000,000 |

Section 32Passive war | |||

| Adult below 70 years | $200,000 | $300,000 | $500,000 |

| Adult 70 years & above | $40,000 | $60,000 | $80,000 |

| Child | $70,000 | $100,000 | $120,000 |

| Family | $540,000 | $800,000 | $1,240,000 |

| Sum insured per insured person per trip | |||

|---|---|---|---|

| Standard Flex Plan | Elite Flex Plan | Premier Flex Plan | |

Section 33Adventure and sports cover | |||

| Adventurous activities Extends the policy to cover for leisure and non-competitive activities like bungee jumping, parasailing, tandem sky diving, canoeing, scuba diving, winter sports, mountaineering up to 3,000m and more | Covered | Covered | Covered |

| Sports equipment Covers for loss or damage to sports equipment during your journey except during use. Covered equipment include snorkel or diving mask, wakeboard, skis, snowboards, fishing tackle equipment, bicycle and more | $100 | $200 | $300 |

| Sum insured per insured person per trip | |||

|---|---|---|---|

| Standard Flex Plan | Elite Flex Plan | Premier Flex Plan | |

Section 34Golfer's cover | |||

| Damage or loss of golf equipment Pays for loss or damage to the golfing equipment during the journey except during use | $1,000 $300 per article | ||

| Hired golf equipment Pays for the cost of hired golf equipment if yours is lost or damage during the trip | $300 $100 per day | ||

| Unused green fees due to injury or illness Pays for unused prepaid green fees if unable to play due to injury or illness | $500 | ||

| Hole-in-one Pays for celebratory drinks expenses when scoring a hole-in-one achievement | $500 | ||

| Sum insured for the first insured person per trip | |||

|---|---|---|---|

| Standard Flex Plan | Elite Flex Plan | Premier Flex Plan | |

Section 35Rental vehicle coverImportant condition | |||

| Rental vehicle cancellation Pays for costs incurred due to cancellation of rental vehicle booking | $300 | $700 | $700 |

| Rental vehicle excess Pays for the excess amount legally payable for rental vehicle damage | $500 | $1,200 | $1,200 |

| Returning a rental vehicle Pays for costs to return a rental vehicle due to injury or illness | $300 | $700 | $700 |

| Sum insured per insured person per trip | |||

|---|---|---|---|

| Standard Flex Plan | Elite Flex Plan | Premier Flex Plan | |

Section 36Cancel for any reason (CFAR)Allows you to cancel, postpone, replace traveller or cut short the trip due to any reason such as work or personal emergencies and receive partial reimbursement. Important conditions Benefits not payable due to government restrictions, war, radioactive contamination, political risks, cyber incidents and pandemics. Refer to exclusions for more details | |||

| Travel cancellation (CFAR) | $2,000 | $4,000 | $6,000 |

| Travel postponement (CFAR) | $300 | $500 | $1,000 |

| Replacement of traveller (CFAR) | $300 | $500 | $1,000 |

| Unused entertainment ticket (CFAR) | $100 | $200 | $300 |

| Shortening the trip (CFAR) | $1,000 | $2,000 | $3,000 |

| Co-payment | We will pay 50% of covered expenses up to the sums insured under this section | ||

| Sum insured per insured person per trip | |||

|---|---|---|---|

| Standard Flex Plan | Elite Flex Plan | Premier Flex Plan | |

Section 37Pre-existing medical condition coverPays for inpatient hospital charges, visit by family member and emergency medical evacuation due to acute onset of pre-existing medical condition during the trip Important Conditions

| |||

Overseas medical expenses | |||

| Adult below 70 years | $75,000 | $100,000 | $150,000 |

| Adult 70 years & above | $50,000 | $75,000 | $100,000 |

| Child | $50,000 | $75,000 | $100,000 |

Emergency medical evacuation and repatriation | |||

| Adult / Child | $100,000 | $150,000 | $200,000 |

Compassionate and hospital visit | |||

| Adult / Child | $3,000 $200 per room per night | $4,000 $300 per room per night | $6,000 $400 per room per night |

| Sum insured per trip | |||

|---|---|---|---|

| Standard Flex Plan | Elite Flex Plan | Premier Flex Plan | |

Section 38COVID-19 CoverPays for cancellation or disruption of the trip and overseas medical expenses due to COVID-19 | |||

Pre-trip benefits | |||

Travel cancellation | |||

| Adult / Child | $3,000 | $4,000 | $5,000 |

| Family | $7,500 | $10,000 | $12,500 |

Travel postponement | |||

| Adult / Child | $500 | $1,000 | $1,500 |

| Family | $1,250 | $2,500 | $3,750 |

Replacement of traveller | |||

| Adult / Child | $500 | $750 | $1,000 |

| Family | $1,250 | $1,875 | $2,500 |

| Sum insured per trip | |||

|---|---|---|---|

| Standard Flex Plan | Elite Flex Plan | Premier Flex Plan | |

During trip benefits | |||

Overseas medical expenses | |||

| Adult below 70 years | $75,000 | $150,000 | $$250,000 |

| Adult aged 70 and above | $37,500 | $75,000 | $100,000 |

| Child | $37,500 | $75,000 | $100,000 |

| Family | $225,000 | $450,000 | $700,000 |

Medical & travel assistance services | |||

| Adult / Child | Included | ||

Emergency medical evacuation and repatriation | |||

| Adult / Child | $1,000,000 | $1,000,000 | $1,000,000 |

| Family | $3,000,000 | $3,000,000 | $3,000,000 |

Shortening the trip | |||

| Adult / Child | $3,000 | $4,000 | $5,000 |

| Family | $7,500 | $10,000 | $12,500 |

Travel disruption | |||

| Adult / Child | $1,000 | $2,000 | $3,000 |

| Family | $2,500 | $5,000 | $7,500 |

Automatic extension of cover | |||

| Adult / Child | Included | ||

Single Return Trip

Annual plan

Individual

Group

Enjoy lower premiums for Child Cover and additional discount for groups with 3 or more travellers.

| No. of travellers | Group discount |

| 3 - 10 travellers | 5% |

| 11 - 20 travellers | 10% |

Family

Single return trip

Simply select your travel destination country based on Area A, B or C. For example, if you are travelling to Japan, you will also be covered for all countries listed under Area B. For travel to multiple countries, select the furthest country.

Annual plan

Select Area A, B or C based on the furthest destination country that you intend to travel to in the coming year.

Area A

Brunei, Cambodia, Indonesia, Laos, East & West Malaysia, Myanmar, Philippines, Thailand and Vietnam.

Area B

Australia, China (except Inner Mongolia and Tibet), Hong Kong, India, Japan, Korea, Macau, New Zealand, Sri Lanka, Taiwan and including countries in Area A.

Area C

Worldwide including countries in Areas A and B.

Important conditions for cover to operate

TravelEasy Flex does not cover:

There are good reasons to get your travel insurance once you have booked your trip as this can protect your pocket if your trip is disrupted due to unexpected events such as strikes, riots and natural disasters that happen at your planned destination.

These events can affect your cover depending on when you have purchased the policy.

TravelEasy Flex covers for insured events that occurs within 30 days before the start of your trip. The insured events are listed under each benefit section (e.g. Travel cancellation) of the policy.

With Cancel for any reason optional cover added, this enhances your policy to give you flexibility to cancel, postpone or replace the traveller for any reason such as work or personal emergencies up to 270 days before the start of the trip and be covered for up to 50% of your incurred expenses. Make sure you purchase your travel policy with this optional cover within 14 days of your initial booking booking of your trip to qualify for this cover.

Should a major event affect your trip, you can refer to the general guideline below.

For policies purchased after the insured event has happened

Event that has already happened or has been made known by the media or authorities before you purchase the policy or booked the trip (for annual plan) are not covered. These are considered as known events.

For policies purchased before the insured event happened and you have not yet departed

| If you have purchased | TravelEasy Flex | TravelEasy Flex with Cancel for any reason optional cover |

| The policy covers for trip cancellation and postponement | ||

| Due to insured event that happens within 30 days before your trip. | Covered | Covered |

| Due to any reason such as work or personal emergencies that happens after you purchase the policy and within 270 days before the start of the trip. | Not covered | Covered |

If you are unsure whether the overseas event affects your trip, please contact your providers (airline, transport, tour, accommodation) to check if your bookings are affected by the event.

If your trip is unavoidably cancelled or postponed, please submit your claim to us and we will assess it based on policy terms and conditions.

Should you decide to proceed with the trip, it is important to remember that you are still covered for claims during your trip that are not related to the known event such as baggage delay caused by the airline or loss of personal items due to theft.

The policy does not cover claims due to known event, government restriction, war, nuclear, radioactive contamination, pandemics, and any circumstances which you or any insured person is aware of before the purchase of this policy or arrangement of the trip.

In the case of earthquakes, they are normally accompanied by aftershocks which may last for weeks after the initial earthquake. If you have purchased your policy after the initial earthquake, you will not be covered for claims relating to the earthquake and their aftershocks as they would be considered as known event which are excluded from cover.

For information on claims procedure, click here.

If you would like to clarify on your coverage, you can chat with Mae or contact us.

| No. | Questions & Answers | |

|---|---|---|

| 1 | Who is suitable to purchase TravelEasy Flex? TravelEasy Flex is suitable for travellers who want the flexibility to customise their protection according to their travel needs and budget. Travellers can choose from 3 plans and 6 optional covers. For more details on coverage differences of TravelEasy, TravelEasy Flex and TravelEasy Pre-Ex, please refer to Compare section below. | |

| 2 | Can foreigners purchase travel insurance? Foreigners holding an employment pass or work permit and living in Singapore can apply, as long as it is for a round trip starting and ending in Singapore within the travel insurance period. | |

| 3 | Can I purchase TravelEasy Flex for my child if I am not travelling with my child? Yes, you can make payment for your child (aged 1 month to below 23 years) by applying as policyholders and indicating your child as the insured person. However, please note that children under 12 years old must be accompanied by a parent or adult guardian for any trip. Children 18 years and above can also apply on their own as policyholder. Payment can be made by the parent. Child under individual plan will have the same benefits and premiums as adults. | |

| 4 | Up to what age can my child be covered under Family plan? Children aged 1 month to up to below 23 years can be covered under the Family plan. | |

| 5 | Can a person aged 70 years and above buy travel insurance for a single trip or an annual travel plan? Single Trip – Yes, all plans | |

| 6 | Can I purchase travel insurance if I am already overseas? No, our travel insurance does not cover trips that have already started or do not begin from Singapore. | |

| No. | Questions & Answers | |||||||

|---|---|---|---|---|---|---|---|---|

| 7 | Are there any differences between family cover and group cover? Family cover Under a family annual policy, the persons insured need not travel together on a trip. However, a child below 12 years must be accompanied by a parent or adult guardian for any journey. Benefits and coverage limits for adult and child vary. Please refer to the benefit table for details. Group cover

You can choose to cover children aged 1 month to below 23 years under child cover or adult cover for higher protection. To insure the child under adult cover, simply include the child under the number of adults. The policyholder must be at least 18 years or old and travelling together on the same trip. | |||||||

| 8 | How do I indicate if I’m travelling to multiple countries for a Single return trip? For Single return trip plan, indicate the furthest country from Singapore for your trip and you will automatically be covered under other countries listed under the relevant Area. For example, if you are travelling to Japan, you will automatically be covered for other countries under Area B. If you are travelling to multiple countries which involves returning to Singapore and departing from Singapore again to the next destination, you need to purchase a separate policy for each trip departing and returning to Singapore as the trip ends once you return to Singapore. For example, if you are travelling to Thailand and returning to Singapore before setting off to USA, it will be considered as two trips, and you will need to purchase two travel insurance policies to cover each trip separately. Area A: Brunei, Cambodia, Indonesia, Laos, East and West Malaysia, Myanmar, Philippines, Thailand and Vietnam. Area B: Australia, China (not including Inner Mongolia and Tibet), Hong Kong, India, Japan, Korea, Macau, New Zealand, Sri Lanka, Taiwan and including countries in Area A. Area C: Worldwide, including countries in Areas A and B. | |||||||

| 9 | Which Area should I choose for annual plan? Choose the Area based on the furthest countries you intend to travel in the year ahead: Area A: Brunei, Cambodia, Indonesia, Laos, East and West Malaysia, Myanmar, Philippines, Thailand and Vietnam. Area B: Australia, China (not including Inner Mongolia and Tibet), Hong Kong, India, Japan, Korea, Macau, New Zealand, Sri Lanka, Taiwan and including countries in Area A. Area C: Worldwide, including countries in Areas A and B. | |||||||

| 10 | Are there any countries excluded from cover? All countries are covered unless expressly excluded. | |||||||

| 11 | Does TravelEasy Flex provide cover for cruise travels? Yes, TravelEasy Flex covers your cruise trip departing from Singapore or an overseas country, as long as the entire trip begins and ends in Singapore. Please indicate the furthest country from Singapore for your trip and you will automatically be covered under other countries listed under the relevant Area. For cruise to nowhere departing from Singapore (meaning, the cruise is not making any stopover at any port/country), please state country of travel as Malaysia for Single return trip. Cruise to nowhere is covered for all annual plans. | |||||||

| No. | Questions & Answers | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 12 | When does the travel insurance cover commence and end for each trip? Cover starts from the time you leave your home or workplace in Singapore to begin the trip abroad and ends 3 hours after your return to Singapore or on the expiry of your travel insurance, whichever is sooner. | |||||||||||||

| 13 | Does MSIG's travel insurance provide cover if the travel agency goes bankrupt? Yes, TravelEasy Flex will cover all irrecoverable travel fares or travel deposits up to the plan limit if a Singapore Tourism Board (STB) registered and Singapore licensed travel agency becomes insolvent before your trip starts, provided the travel insurance is bought at least 3 days before the departure date and the insolvency does not take place before you purchase your travel insurance policy. | |||||||||||||

| 14 | Do the optional covers automatically protect all the travellers insured in the policy? Can I specify the optional cover to protect specific travellers? For Group and Family cover under the TravelEasy Flex, the optional cover benefits apply differently when selected as shown below.

| |||||||||||||

| 15 | For rental vehicle optional cover, can any traveller rent and drive the rented vehicle? No, it only applies to the vehicle rented by the first traveller named in the policy. However, any traveller insured in the policy can drive the rented vehicle if they are authorised drivers under the rental agreement and hold a valid driving license for the destination country. | |||||||||||||

| 16 | For rental vehicle optional cover, does it cover if I rent more than 1 vehicle during the trip? Yes, the rental vehicle optional cover allows the first traveller named in the policy to rent multiple vehicles during the trip, but not more than one at the same time. For example, if you are traveling for a 10-day trip and you rent a vehicle from day 1 to day 3 and another vehicle from day 6 to day 9, both rental vehicles will be covered. However, if you rent two vehicles from day 1 to day 3, you will not be covered for both vehicles as this falls outside the policy conditions, and neither vehicle will be covered. | |||||||||||||

| 17 | For rental vehicle cover, does it cover me if I rent motorbikes? The rental vehicle optional cover only applies to cars and campervans rented by the first traveller named in the policy. Rental motorcycles are not covered | |||||||||||||

| 18 | How does Cancel for any reason optional cover work? Cancel for any reason cover is only available for Single return trip policy. To be eligible, buy the policy with this optional cover within 14 days of your first booking for your trip, such as for a tour, transport, accommodation, or entertainment ticket. This optional cover allows you to cancel, postpone, replace a traveller, or cut short the trip for any reason, such as work, health conditions or personal emergencies, and receive partial reimbursement. For example, if you have a sudden work commitment or a personal emergency that prevents you from traveling, you can use this cover to get back up to 50% of your incurred expenses up to the sums insured. However, there are situations that are not covered, such as government restrictions, war, terrorism, radioactive contamination, political risks, cyber incidents, and pandemics. | |||||||||||||

| 19 | Is COVID-19 covered under TravelEasy Flex? Yes, if you select the COVID-19 optional cover, you are covered for benefits such as overseas medical expenses, trip cancellation, and travel disruption due to COVID-19. | |||||||||||||

| 20 | Is pre-existing medical condition covered? Yes, with the pre-existing medical condition optional cover for Single return trips for travel duration up to 30 days. When this optional cover is selected, the specified traveller will be covered for unexpected and hefty expenses such as overseas medical expenses and emergency medical evacuation if there is a sudden deterioration of their pre-existing medical condition during the trip. To be eligible, the traveller must meet all the following conditions:

However, terminal illness, HIV, sexually transmitted diseases, pregnancy, and related conditions and mental illness are not covered. | |||||||||||||

| 21 | For Pre-existing medical condition optional cover, must I provide information on all my pre-existing medical conditions or produce a doctor's report? You do not need to furnish such information. You are eligible to apply so long as you meet the conditions mentioned under FAQ 21. | |||||||||||||

| 22 | Is business trip covered under TravelEasy Flex? Yes, TravelEasy Flex covers you for business travel, excluding claims arising from manual work and legal liability resulting from business activities. | |||||||||||||

| No. | Questions & Answers | |

|---|---|---|

| 23 | How can I obtain an unencrypted (non-password protected) TravelEasy Flex ePolicy for submission to the authorities of the country I am travelling to? You may download an unencrypted copy of your TravelEasy Flex ePolicy from mConnect Customer Portal. | |

| 24 | Can I extend the period of cover if I decide to extend my trip whilst overseas? Yes, provided there are no known circumstances or events likely to lead to a claim, subject to a minimum premium of $10. Please email [email protected] with the following information:

We will reply your email within 3 working days on the additional premium payable if we agree with the extension, and will only proceed with the extension upon receipt of your payment. | |